Michael Burry Just Bought This Stock!

Michael Burry Just Bought This Stock!

One investor I follow extremely close is Michael Burry as his value investing strategy is similar to mine. He is a great investor and tend to look at companies off the beaten path.

Back in the day Burry wrote a value investing blog while going to medical school. Legendary investor Joel Greenblatt followed the blog and encouraged Burry to start a hedge fund. The blog is no longer around but someone put together a DropBox of his prior writeups.

The writeups are incredible and if you pour through them, you can see the value investing strategy that Burry uses to outperform the market. Burry invests in obscure companies trading at a meaningful discount to fair value.

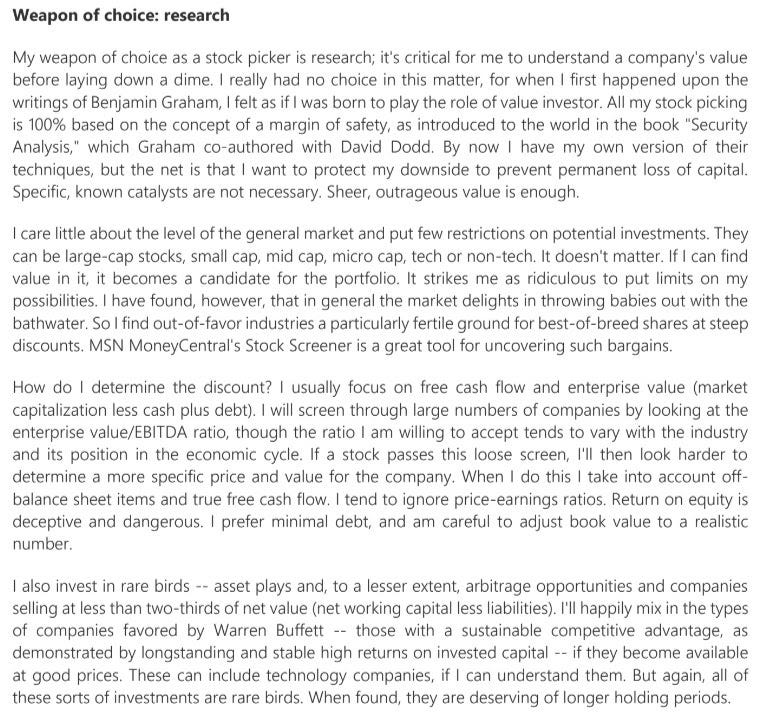

Check out a portion of this writeup he wrote back in the day as an example.

I wanted to spend the rest of the day highlighting a stock that Michael Burry owns and the reason why he owns it. I’ve followed this company for years given the one-of-a-kind owned real estate, high barriers to entry, government contracts and hidden growth business with almost zero competition. The business is dirty, not ESG friendly and there is a ton of debt on the balance sheet — which gives value investors not worried about investing in ESG friendly companies — an opportunity to invest in a company trading meaningfully below tangible replacement value.

This company has rallied significantly from the all-time lows once seen a year ago and has subsquently fallen back down to basement level valuations. Despite the move in the stock price, the valuation is still compelling and trades at a meaningful discount to fair value. Debt has been refinanced. Assets have been sold. And the hidden growth business is firing on all cylinders with 50% operating margins. I’m bullish on the company and own it. As Michael Burry once famously wrote, research is his weapon of choice in the public markets. I’ve done a lot of research on this company and think the situation is compelling enough to write about it today. Let’s take a stab at the setup here.

The Geo Group, Inc. (GEO)

A company beaten down by too much debt, lost government contracts at the core business, dividend investors who bailed when the corporation went through a de-REIT, an unfriendly political environment and ESG concerns with the risk of financial firms not banking the industry. Despite the negative backdrop, management was able to refinance the large outstanding debt, sell real estate assets, grow a tech segment with 50% operating margins and zero competition and has plans to de-lever the balance sheet by $200 million per year. Replacement value of the real estate is meaningfully higher than the current enterprise value and the segment with tech level margins could be sold for the entire value of the enterprise today.

The Geo Group is an owner and operator of for-profit private prisons. The market cap is $1.4 billion and enterprise value are $3.2 billion. Operations across the globe include 86,000 beds at 106 facilities and an electronic monitoring and supervision segment that serves over 300,000 individuals.

The core assets are the owned and operated prisons that generate $450 million of EBITDA per year. The prisons are operated by Geo Group under long-term inflation adjusted government contracts that provide Geo Group with a steady stream of revenues and income based on a per prisoner per day basis. On average Geo Group gets $70 bucks per day on beds they own and $50 bucks per day on managed beds. 80% of costs are fixed, giving this business extremely high operating leverage for every incremental prisoner housed.

GEO owns 50,000 beds and manages 100 facilities in total. The replacement value of a prison is significant and continues to increase in value every year as it becomes harder to build a new prison from the ground up due to imposing regulations and NIMBY issues. As an example, a proposed new-build prison in Alabama is estimated to cost at least $1.3 billion with 4,000 beds, or a cost per bed of $325,000. The new build has been axed due to political activists getting involved and lenders pulling out on the deal due to ESG concerns.

This shows the replacement value of the prisons Geo Group owns is substantial and likely worth more than the current enterprise value of only $2.8 billion. With a replacement cost per bed of $100-325k, Geo Group’s owned prison replacement cost is in the range of $5-16 billion. The replacement cost will only increase in time as older and less efficient federal and state run prisons continue to shut down or fall apart and materials, labor and construction costs continue to increase from inflationary pressures.

We probably won’t see anyone coming in to buy up these prisons anytime soon, but the replacement cost provides a strong margin of safety for investors. Should Geo Group need to free up additional liquidity, they would continue to piece-meal sell certain prisons to paydown debt, like we have saw in the last two years as the management team focuses on free cash flow and de-levering and de-risking the business from outside financers.

The other portion of the thesis is the high growth and margin BI Incorporated. BI Incorporated is an owned and operated tech platform that allows Geo Group to electronically monitor paroles and illegal immigrants with an app on a phone. The business is extremely high margin with 50% operating margins. Revenues have grown over 80% this year and should be at least flat this year with a potential revenue kick if Title 42 is released.

The federal program Geo Group won is a five-year exclusive contract with ICE, starting in August 2020, that gives Geo Group 100% of the revenues dedicated to monitoring illegal immigrants through phones, instead of housing the immigrants in facilities or putting tethers on their ankles. The Biden administration is pushing hard on this program as it gives illegal immigrants more freedom in their day to day lives (check in remotely on their phone via Facetime with their parole officer) and costs much less than housing and feeding them in federal facilities.

Revenues have grown over 80% this year and Geo monitors over 350,000 individuals with the technology. Revenues for 2022 were $500 million and sports $300 million of EBITDA. Capex is extremely minimal ($16 million in 2022) and there is literally zero competition for the next five years. The business model should also be relatively sticky after the contract is complete as it would be extremely difficult to switch technologies on 600,000 individuals to another provider overnight. As Geo continues to cement their way into this market, I suspect they will sign additional contracts with federal agencies and rollout more incremental products, further building a competitive moat.

High growth and margin business like BI Incorporated should be valued at least 10-15x EBITDA. By the end of 2023, BI Incorporated will be generating $350-400 million of EBTIDA, giving the segment a value of $3.5-5.2 billion. I expect this EBITDA to only grow as the technology is adopted and Geo continues to penetrate new markets like monitoring recently released prisoners.

Catalysts include the removal of Title 42, expected May 11, 2023, which will allow a massive number of Hispanic immigrants to cross the border for the first time since 2020 into the United States. With Title 42, immigrants are immediately turned around back into Mexico due to COVID-19 protocols. It is estimated that they are 100,000 to 150,000 immigrants per months at the southern border (normal numbers are under 20,000) and will provide a massive influx of individuals into the United States. Geo Group is well equipped to handle the influx of individuals with owned facilities (remember 80% incremental margins) and BI Incorporated should they run out of space.

Other catalysts are a sale or spin-off of BI Incorporated and the de-leveraging of the stock as management has guided to add $200 million of cash to the balance per year (this is a conservative estimate and could be well north of management’s estimate) and use this cash to paydown debt. Once under 3.5x debt-to-EBITDA Geo will consider returning capital back to shareholders. I expect Geo to be meaningfully under 3.5x debt-to-EBITDA by the end of 2023, should my forecasts prove accurate. A return of a quarterly dividend will bring back income-oriented investors. As a note, Geo Group was trading north of $30 per share when they were a dividend paying REIT and BI Incorporated was non-existent.

Risks

Geo Group is highly levered with over $2 billion of debt. $1 billion of this debt is floating rate and will be subjected to higher interest rates. Interest expenses will be close to $220-250 million per year and any downturn in the business will result in significant de-leveraging.

Despite the push of electronic monitoring from the Biden administration, the administration is against private prisons and has removed all contracts with private prisons with USMS. Additional push back or loss of contracts is a major risk.

Geo Group had a tough time refinancing their debt given that banks and finance firms are unwilling to bank private prisons. As long as there is debt outstanding, Geo is at risk of becoming un-bankable.

BI Incorporated is the growth engine with high margins. Competitors like CoreCivic are building similar technologies and there is likely to be competition in the future. A loss of a key contract could significantly depress revenues and profitability.

An investment in Geo is an investment in a private prison, which comes with ethical hurdles and risks.

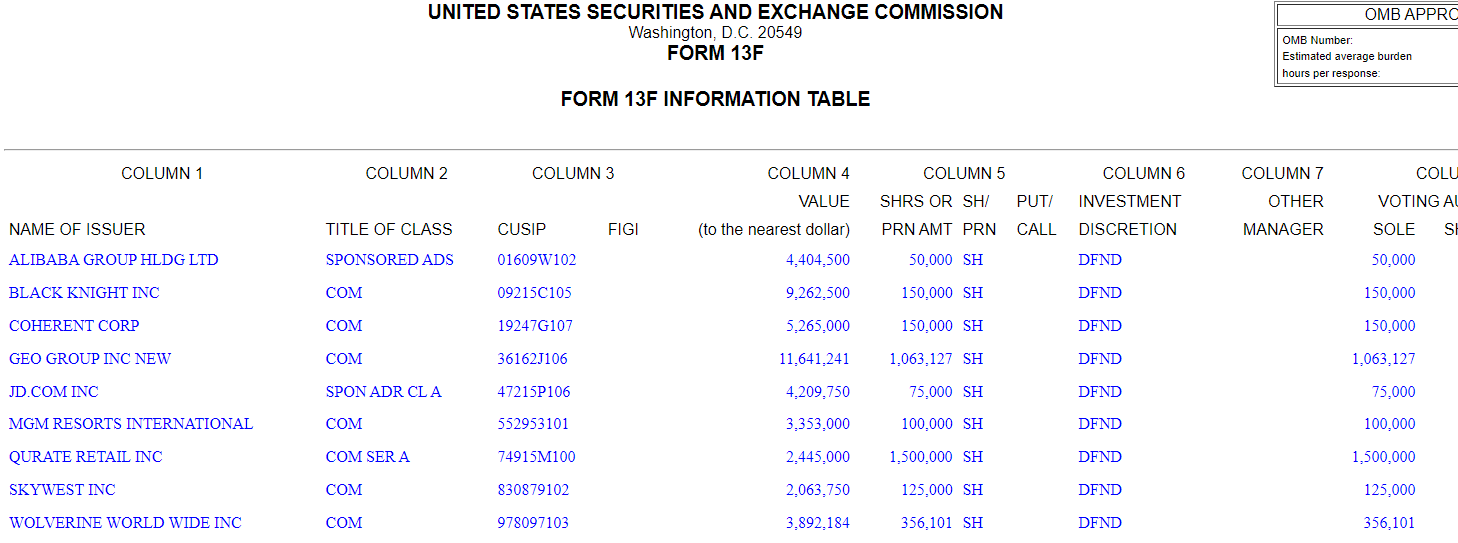

Michael Burry owns over 1 million shares of Geo Group making it his single largest public holding with a value of over $15 million. Based on my research I am bullish on Geo Group and think the company provides a large margin of safety based on owned real estate, the successful refinancing of the debt, management’s forecasts on cash flows, future de-levering of the balance sheet and the growth at BI Incorporated. I am long Geo and will add on any pullback.